Imagine driving a car with no brakes and no map. That is exactly what running a business without a risk assessment feels like. The problem is, thousands of companies still do it. Seasoned business owners know that risks can vary from fast-moving markets to unpredictable tech failures, and they do not wait around. But with the right framework, you can spot them before they cost you everything.

This article breaks down the exact fundamentals that turn risk from a fear into a roadmap.

We will discover

What is Business Risk Assessment?

This indicates the process of checking what could go wrong in a business before it actually happens. It helps owners and managers spot possible problems like money loss, system failure, or legal trouble.

First, they look at different parts of the business, then list out risks, and finally figure out how likely those risks are and what effects they might cause. After that, they choose smart ways to deal with them, either reducing, avoiding, or preparing for them.

This process keeps businesses alert and ready.

Types of Risks Businesses Face

Strategic

Strategic risks occur when market conditions change or competitors suddenly act in ways that affect your plans. For example, a new brand might launch a cheaper version of your product, forcing you to rethink pricing or product quality. These risks make businesses change direction quickly to stay relevant.

Operational

These risks show up in day-to-day tasks. These include broken systems, late deliveries, or staff mistakes. If a supplier fails to send materials on time, production stops, customers wait longer, and profits drop. Human error, like miscommunication or skipping safety steps, can also lead to big losses. These issues create delays and stress.

Financial

Financial risks hit when money matters go sideways. These can include rising interest rates, bad loans, cash shortages, or changing currency values. If a business borrows money and cannot pay it back on time, it faces serious trouble. Plus, when customers delay payments or when prices jump unexpectedly, it becomes hard to keep the books balanced.

Compliance and Legal

These sorts of risks appear when rules change or when businesses break contracts. Governments can update laws anytime, and if businesses miss something, they can face fines or lawsuits. For instance, using outdated tax rules or skipping safety codes can quickly land a company in hot water. Also, not honouring agreements with partners can lead to court battles.

Reputational and Cybersecurity

If hackers steal customer data, people stop buying, and the company’s name gets dragged online. Even one mistake on social media or a poor product review can cause a storm. This is why businesses need to protect their systems and speak honestly with their audience. When people trust a brand, they stick with it.

Fundamentals of Risk Assessment

Identify

This lays the first step. This is where businesses look around and spot what might go wrong. They examine different areas like finance, operations, and technology to uncover possible threats. These risks could include system failures, supplier delays, or even changes in customer behaviour.

It is quite challenging, as leaders must ask the right questions and involve people from different teams to catch risks early. Instead of assuming things will go smoothly, they should use sharp thinking to map out what could derail plans.

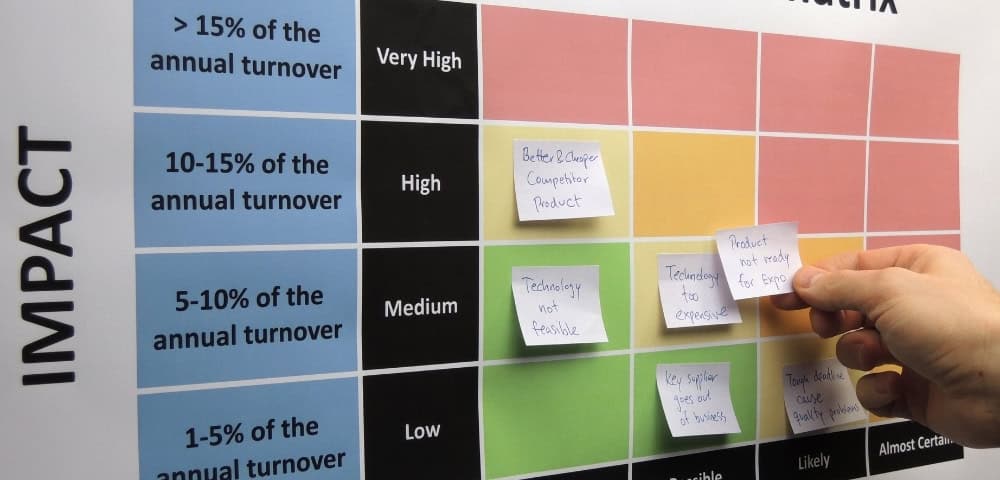

Quantify

After finding the risks, businesses cannot stop there. Instead, they need to measure how serious each one is.

They must figure out how likely something is to happen and how much damage it could cause if it does. This step adds weight to the risks so they do not treat a minor glitch the same as a major threat. This is where managers use numbers, scores, or even heat maps to mark the impact.

This clear thinking helps remove guesswork and adds real meaning to their decisions. When businesses see the size and shape of a risk, they can act with more focus and less confusion.

Prioritise

Now that businesses know which risks exist and how big they are, they must sort them. This means lining up the most dangerous or most likely ones at the top and handling smaller ones later.

If they treat all risks the same, they might waste time or miss urgent problems. So, they put their energy where it counts most. This smart order helps them act faster, save money, and protect key parts of the business.

In the rush of daily work, prioritising risks keeps teams focused and prevents panic when things start to go sideways.

Evaluate

Once businesses list and sort their risks, they step back and ask if their current plans make sense. They study whether their existing rules, tools, or habits can handle the risks or if they need changes. If something seems too risky with the current setup, they flag it for improvement.

This stage gives a deeper view. If you look closer, it is not just about knowing what could happen, but really asking, ‘Are we ready for this?’.

Good evaluation connects risk levels with real business goals, helping decision-makers stay alert and ready instead of getting caught off guard.

Mitigate and Manage

After understanding the risks, businesses shift into action mode.

They pick the best ways to reduce or handle each risk. Maybe they change a process, add a backup plan, or train their staff better. Sometimes they avoid a risk completely or share it through insurance.

What you need to understand is that managing risk means choosing smart responses instead of ignoring the problem. It also means keeping people responsible for each step.

When businesses take charge of risks, they avoid chaos, stay productive, and create more confidence across the team. This part turns planning into real-world protection that keeps everything on track.

Monitor and Review

Risks do not stay the same forever, so businesses need to keep watching.

Even if they build solid plans, things like new laws, tech updates, or staff changes can shift the risk landscape. That is why reviewing risk plans regularly matters. Your employees will check what is working, what needs updates, and what new issues have popped up.

They also learn from mistakes or close calls. Keeping their eyes open helps businesses stay ready for anything. Not just once, but all the time. This habit builds a steady rhythm where risk management becomes part of everyday thinking, not just a one-time task.

Why is Risk Assessment Important for a Business?

Improves Decision-Making and Strategic Planning

Risk assessment gives leaders a clear view of what might go wrong and where new chances might appear.

Instead of making random guesses, they rely on solid facts to guide decisions. When businesses understand risks, they can plan smarter. This kind of thinking helps teams focus on what really matters.

As strategies shift or new goals come up, having a list of known risks makes it easier to adjust.

Enhances Business Continuity and Resilience

When businesses know what might go wrong, they can prepare before disaster hits. Risk assessment helps them build backup plans so they do not freeze up during a crisis.

Whether a fire breaks out, a supplier fails, or a system crashes, they already know what steps to take next. This keeps the business running even during messy situations. Instead of falling apart, they stay strong and bounce back faster.

That steady rhythm means customers stay happy, workers stay productive, and the business does not lose its balance every time trouble knocks on the door.

Ensures Legal and Regulatory Compliance

Rules change, and industries expect businesses to follow the latest laws. If companies miss updates or ignore risks, they can face big fines or legal trouble.

This is when the latter helps leaders catch areas where they might break the rules and fix them before anyone calls them out. It also shows that the business takes its responsibilities seriously. When auditors or inspectors show up, they find that everything runs smoothly.

As you can see, staying ahead of regulations saves money, protects reputation, and keeps the company out of long, painful court battles.

Reduces Financial Losses

‘Risks’ is another name for ‘money eaters.’ Whether it is a cyberattack, a broken machine, or a deal gone wrong, the cost of fixing a mess often hurts more than preventing it.

Risk assessment helps businesses catch those problems early and either reduce them or stop them completely. When leaders fix weak spots in advance, they save on damage control, insurance premiums, and lost revenue.

Instead of watching money disappear into avoidable mistakes, they keep more of it working toward their goals. Prevention always costs less than a messy cleanup later.

Builds Stakeholder Confidence

People want to trust a business that looks ahead and stays ready. Whether they are investors, employees, or customers, they feel safer when a company handles risk with care. This sort of assessment proves that the business does not just hope for the best; it plans for the worst and handles it calmly.

That kind of preparation makes people stick around. Investors feel their money is in smart hands, customers know the service will not drop, and employees feel confident in their roles.

Discovering Business Risks Early with AI-Powered Tools

Every risk is sending you a signal. You may not be listening, yet Artificial Intelligence hears it first. This is why you need to hold hands with AI-powered tools. Tigernix presents an AI-driven Business Intelligence Platform, and with this, you no longer have to scramble in the dark. Now you can act with precision. Let AI power your next smart move.